Buying a home is not just a lifestyle decision — it’s one of the smartest long-term financial investments you will ever make. In India, government-backed tax deductions make homeownership even more attractive, especially for young professionals, salaried individuals, and first-time buyers looking for affordability and financial stability.

Whether you’re planning to buy an affordable home, a mid-segment apartment, or exploring premium developments like Sarang by sumadhura, knowing the Tax Benefits on Home Loans can drastically reduce your tax burden and make EMIs more manageable. This expanded Guide for First-Time Buyers explains every tax advantage in detail, helping you make financially sound decisions.

Why Understanding Tax Benefits Is Essential for First-Time Buyers

The Indian government encourages homeownership through a variety of tax deductions. These benefits help first-time buyers save lakhs over the loan tenure.

Major Reasons Tax Benefits Matter

- Reduce yearly tax liability significantly

- Increase monthly take-home salary due to lowered tax outgo

- Make EMIs more affordable by reducing the effective interest burden

- Boost financial stability for new homeowners

- Encourage long-term investment in real estate

Most first-time buyers are unaware of the full extent of these advantages — understanding them can transform your financial planning.

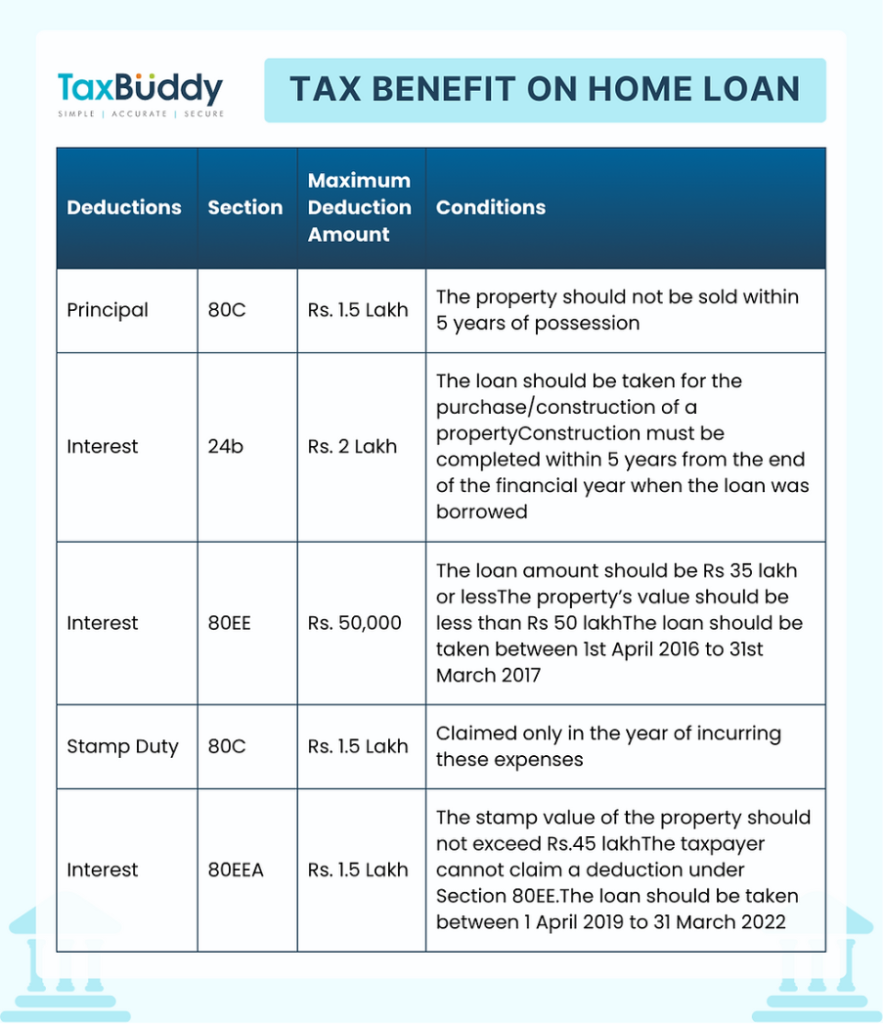

Section 80C — Tax Deduction on Principal Repayment

Under Section 80C, you can claim a deduction for the principal portion of your home loan EMIs.

Key Highlights

- Maximum deduction allowed: ₹1,50,000 per financial year

- Covers:

- EMI principal

- Stamp duty

- Registration charges

- Applicable for self-occupied and rented properties

Conditions to Remember

- Benefit available only after construction completion

- The property cannot be sold within 5 years of possession

- If sold earlier, deductions claimed will be reversed

This section alone can reduce your tax liability significantly.

Section 24(b) — Tax Deduction on Home Loan Interest

This section provides major savings on the interest component of your EMIs.

Deduction Limits

- Up to ₹2,00,000 per year for self-occupied homes

- No fixed limit for rented homes (subject to overall ₹2 lakh loss cap)

Pre-Construction Interest

Homebuyers often pay Pre-EMI interest during construction. This amount is also eligible:

- Can be claimed in 5 equal installments after the property is complete

This section is extremely beneficial for homeowners with high loan amounts.

Additional Tax Deductions for First-Time Buyers — Sections 80EE & 80EEA

These deductions were introduced to help first-time buyers purchase affordable homes.

Section 80EE — Extra ₹50,000 Deduction

Eligibility:

- You must be a first-time homebuyer

- Loan value must be below the set limit

- Loan must be from a recognized lending institution

This benefit is in addition to 80C and 24(b).

Section 80EEA — Extra ₹1,50,000 Deduction

Eligibility criteria:

- Property must qualify under affordable housing

- Stamp duty value must not exceed ₹45 lakh

- Buyer should not be claiming 80EE simultaneously

This enhances total tax-deductible interest up to an impressive ₹3,50,000 per year when combined with Section 24(b).

Tax Benefits for Joint Home Loans — Double the Savings

Purchasing a home jointly can double your savings.

How Joint Benefits Work

Each co-owner can claim:

- ₹1,50,000 under Section 80C

- ₹2,00,000 under Section 24(b)

This provides a combined tax deduction of:

₹7,00,000 per year for a couple

A powerful financial planning strategy for new families.

Tax Deductions for Under-Construction Homes

Many first-time buyers choose under-construction homes due to affordability.

Key Rules

- Deductions apply only after completion of construction

- Principal deduction begins only post-possession

- Pre-construction interest can still be claimed — in 5 installments

This makes affordable pre-launch and early-stage bookings even more beneficial.

Tax Benefits for NRI Homebuyers

NRIs enjoy similar tax benefits as resident Indians:

Eligibility for NRIs

- Can claim deductions under 80C, 24(b), 80EE, 80EEA

- Must repay loan via NRE/NRO accounts

- Property must be located in India

NRIs can use these benefits while investing in long-term assets like rental homes, retirement homes, or premium properties.

Real-Life Example — How Much Can You Actually Save?

Let’s assume:

- Annual principal paid: ₹1,50,000

- Annual interest paid: ₹2,20,000

- Eligible for Section 80EE: ₹50,000

Total Tax Deduction Calculation

- 80C → ₹1,50,000

- Section 24(b) → ₹2,00,000

- Section 80EE → ₹50,000

Total Tax Benefit: ₹4,00,000 per YEAR

If you fall in the 30% tax bracket:

Savings = ₹1,20,000 per year

Over 10 years, that’s a huge saving of ₹12 lakh.

Smart Financial Planning Tips for First-Time Homebuyers

Here are the top strategies recommended by Bud Realty:

1. Choose an EMI Structure Aligned with Income Growth

Salaried professionals can opt for step-up EMIs to reduce early burden.

2. Maintain All Loan-Related Documents

Banks issue interest certificates annually — crucial for claiming deductions.

H3: 3. Prefer Joint Loans for Maximum Tax Savings

Ideal for newly married couples or working spouses.

4. Invest in a Property with High Appreciation Potential

Tax benefit + property appreciation = maximum wealth creation.

5. Start Early — Even Small Savings Matter

The earlier you begin repaying a home loan, the more tax benefits you accumulate.

How Bud Realty Supports Homebuyers in Their Tax Planning Journey

Bud Realty ensures that first-time buyers not only find the right property but also fully understand how to optimize tax savings.

Bud Realty Offers:

- Guidance on loan eligibility & bank tie-ups

- Explanation of tax deductions in simple terms

- Assistance in choosing tax-efficient properties

- Support in documentation & financial planning

- Market insights for projects like Sarang by sumadhura

Our goal is to ensure every first-time homeowner benefits fully from every possible deduction.

The Bottom Line

Home loans offer far more than financial support — they provide some of the most substantial tax benefits available to Indian citizens. Understanding these deductions can save you lakhs of rupees, reduce stress, and make homeownership far more accessible.

With proper knowledge of the Tax Benefits on Home Loans, combined with expert guidance from Bud Realty, first-time homebuyers can make confident, well-planned, and financially intelligent decisions.

Buying a home isn’t just a purchase — it’s the beginning of long-term wealth creation.

Add comment